Access to affordable financing remains one of the most critical challenges facing Micro, Small and Medium Enterprises (MSMEs) in Nigeria. Despite contributing significantly to employment and national output, many small businesses struggle to secure structured loans due to high interest rates, lack of collateral, poor credit history, or informality.

To address this funding gap, the Small and Medium Enterprises Development Agency of Nigeria (SMEDAN) collaborates with financial institutions such as Sterling Bank and Jaiz Bank to facilitate access to business loans tailored for MSMEs.

This in-depth guide explains everything Nigerian business owners need to know about the SMEDAN Sterling loan application process, eligibility, documentation, loan portals, interest rates, repayment expectations, and practical approval strategies.

Understanding the SMEDAN Loan Framework

It is important to clarify a common misconception: SMEDAN does not directly disburse loans like a commercial bank. Instead, it plays a facilitative and verification role.

The structure typically works as follows:

- SMEDAN registers and verifies MSMEs.

- Partner banks provide the actual loan funding.

- Loan applications are processed through designated portals.

- Banks conduct credit risk assessment.

- Approved funds are disbursed directly to the business account.

This model strengthens financial inclusion while ensuring proper oversight and risk management.

What Is the SMEDAN Sterling Loan?

The SMEDAN Sterling Bank loan is a structured financing partnership designed to provide affordable credit facilities to MSMEs.

Often referred to as:

- Starling Bank SMEDAN loan

- SMEDAN/ Sterling Bank loan registration portal

- SMEDAN Sterling Bank loan link

- Sterling SMEDAN 5bn loan

This initiative pools funds sometimes in multi-billion-naira tranches to support small business expansion, working capital needs, and operational improvements.

The “5bn” reference typically reflects the size of intervention funding made available for MSME lending under specific program cycles.

Types of SMEDAN-Linked Loan Options

1. SMEDAN Sterling Loan (Interest-Based Financing)

This is a conventional SME loan offered through Sterling Bank. Key features may include:

- Competitive SME-focused interest rates

- Flexible repayment tenure

- Working capital financing

- Equipment or asset acquisition financing

- Structured repayment schedules

The SMEDAN Sterling Bank loan interest rate may vary depending on:

- Central Bank monetary policy

- Risk profile of applicant

- Business sector

- Loan duration

- Collateral availability

Interest rates are generally designed to be more SME-friendly than typical unsecured commercial loans.

2. SMEDAN Jaiz Loan (Non-Interest Financing)

For entrepreneurs seeking Sharia-compliant financing, SMEDAN partners with Jaiz Bank.

The SMEDAN non interest loan follows Islamic banking principles, which means:

- No conventional interest charges

- Asset-backed transactions

- Profit-sharing or markup structures

- Ethical financing guidelines

Search terms often include:

- SMEDAN Jaiz loan requirements

- Jaiz SMEDAN loan portal

- SMEDAN Jaiz Bank loan portal

This option is ideal for entrepreneurs who prefer non-interest banking structures.

Who Can Apply for SMEDAN Loan?

Eligibility is determined by both SMEDAN registration status and partner bank credit criteria. General eligibility requirements for SMEDAN loan include:

- Registered business with CAC

- Active SMEDAN registration (SUIN issued)

- Nigerian citizen or legally operating resident

- Functional business bank account

- Demonstrable business activity

- Acceptable credit history

Micro, small, and medium enterprises across sector, including agriculture, manufacturing, retail, services, and technology may qualify.

SMEDAN Registration Loan Requirement

Before accessing funding, entrepreneurs must complete SMEDAN registration.

This ensures:

- Business inclusion in national MSME database

- Verification of operational status

- Eligibility for structured interventions

Without SMEDAN registration, loan applications may be delayed or rejected.

Step-by-Step: How Do I Apply for SMEDAN Loan?

Many entrepreneurs ask: How do I apply for SMEDAN loan? Here is a comprehensive step-by-step guide.

Step 1: Complete CAC Registration

Your business must be legally registered with the Corporate Affairs Commission.

Required documents include:

- Certificate of incorporation or business name registration

- Company registration number

Step 2: Complete SMEDAN Registration

Obtain your SMEDAN Unique Identification Number (SUIN).

This step strengthens your loan eligibility.

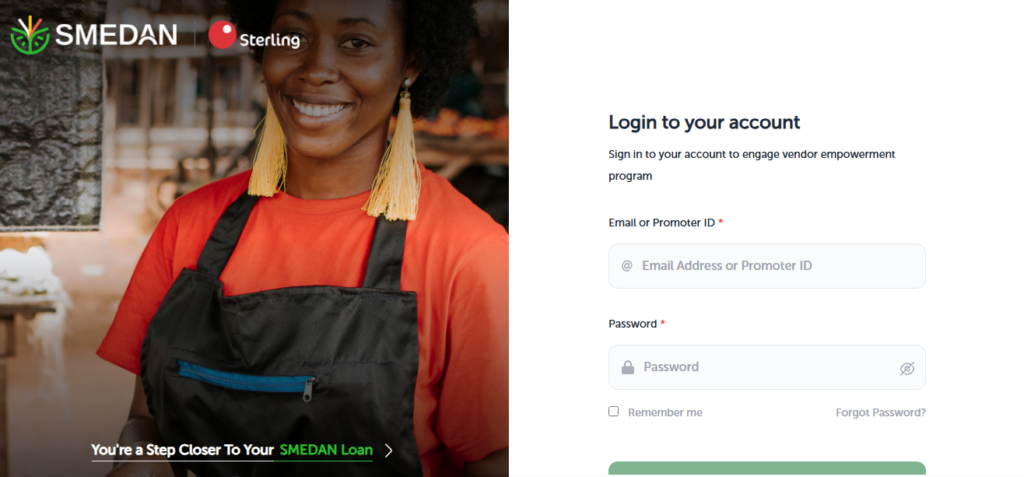

Step 3: Access the Official Loan Portal

Visit the official SMEDAN/ Sterling Bank loan registration portal or Jaiz SMEDAN loan portal through verified channels.

Avoid third-party agents demanding processing fees.

Step 4: Create Account (SMEDAN Loan Login)

You will create an online profile using:

- Email address

- Phone number

- Business details

- BVN

This is often referred to as SMEDAN loan login or SMEDAN Sterling Bank loan portal login.

Step 5: Complete the Online Application Form

Some applicants refer to this as the SMEDAN CBN loan application form.

You will provide:

- Loan amount requested

- Business turnover details

- Purpose of loan

- Employment size

- Operational history

Accuracy is critical.

Step 6: Upload Required Documents

Typical required documents include:

- CAC certificate

- SMEDAN certificate

- Valid ID

- Bank statements (6–12 months)

- Utility bill

- Business plan (for larger facilities)

- Tax Identification Number (TIN)

Sterling SMEDAN loan requirements may also include cash flow projections.

Step 7: Credit Assessment

The bank reviews:

- Credit score

- Cash flow strength

- Industry risk

- Debt exposure

- Loan repayment capacity

Step 8: Approval and Disbursement

If approved, funds are disbursed directly to your registered business bank account.

SMEDAN 1.5m Loan – What You Should Know

The SMEDAN 1.5m loan is commonly referenced as a funding tier designed for micro and small enterprises.

This facility may support:

- Stock purchase

- Equipment upgrade

- Business expansion

- Working capital

Approval depends on financial viability, not just registration.

SMEDAN Personal Loan – Clarification

SMEDAN does not typically provide personal consumer loans.

If you see “SMEDAN personal loan,” it usually refers to:

- Sole proprietorship business loan

- Micro-enterprise loan

- Individual entrepreneur business funding

Funds must be used strictly for business purposes.

Loan Detail – SMEDAN Credit Information Portal

The loan detail-SMEDAN credit information portal supports:

- Verification of applicant data

- Credit assessment transparency

- Monitoring loan performance

- Fraud prevention

Maintaining good credit history improves future approval chances.

SMEDAN Sterling Bank Loan Interest Rate

Interest rates depend on:

- Central Bank policy framework

- Risk assessment outcome

- Loan tenure

- Market conditions

Applicants should confirm updated rates via official SMEDAN Sterling Bank loan link.

How Can I Access My SMEDAN Loan?

If approved:

- Log into the SMEDAN loan login portal

- Confirm approval notification

- Check your business account

- Review repayment schedule

If funds are delayed, contact the partner bank directly.

Common Reasons for Loan Rejection

Applications may be rejected due to:

- Incomplete documentation

- Poor credit history

- Inconsistent bank statements

- Unverifiable business activity

- Inflated financial projections

- Incorrect portal submission

Proper preparation improves success rates.

How to Improve Your Approval Chances

Securing a SMEDAN-linked loan requires more than simply completing an online application. Financial institutions assess risk carefully, so preparation and transparency significantly improve your chances of approval.

To strengthen your SMEDAN loan online application, consider the following strategies:

1. Maintain Clean Financial Records

Accurate and organized financial records demonstrate professionalism and stability. Keep proper documentation of income, expenses, inventory, payroll (if applicable), and tax filings. Clear financial statements help partner banks such as Sterling Bank or Jaiz Bank evaluate your business performance confidently.

2. Separate Personal and Business Finances

Operate a dedicated business bank account. Mixing personal and business transactions creates confusion and makes it difficult for lenders to assess true cash flow. A separate account strengthens credibility and simplifies credit assessment.

3. Build Strong Transaction History

Consistent business activity reflected in your bank statements increases lender confidence. Regular deposits, supplier payments, and operational transactions show that your business is active and generating revenue.

4. Avoid Excessive Existing Debt

High outstanding loans or frequent overdrafts may signal financial stress. Before applying, reduce unnecessary liabilities where possible. Lower debt exposure improves your debt-to-income ratio and risk profile.

5. Submit a Realistic Loan Request

Requesting an amount that aligns with your business size and repayment capacity increases approval likelihood. Inflated loan requests without supporting revenue history may lead to rejection.

6. Provide a Detailed Business Plan

A clear business plan outlining your operations, revenue model, target market, and how the loan will be utilized shows preparedness. Lenders want to see that funds will generate income sufficient for repayment.

7. Maintain a Good Credit Score

Your credit history plays a critical role in loan approval. Avoid bounced cheques, unpaid obligations, and defaults. A strong credit profile demonstrates reliability and improves future financing opportunities.

By combining proper documentation, financial discipline, and realistic planning, entrepreneurs can significantly enhance their approval prospects under programs facilitated by the Small and Medium Enterprises Development Agency of Nigeria. Preparation is often the deciding factor between rejection and successful disbursement.

Key Advantages of SMEDAN Sterling Loan Initiative

Access to structured and affordable financing can determine whether a small business survives or scales. The SMEDAN Sterling Loan Initiative is designed to address real funding gaps faced by Nigerian MSMEs while promoting broader economic development.

1. Structured SME Financing

Unlike conventional commercial loans that may impose rigid terms, the initiative offers financing models tailored to the realities of small and medium enterprises. Through collaboration between the Small and Medium Enterprises Development Agency of Nigeria and Sterling Bank, loan structures often feature manageable repayment plans, SME-focused assessment criteria, and flexible tenures that align with business cash flow cycles.

2. Financial Inclusion

Many Nigerian businesses operate informally without access to formal banking services. The SMEDAN-linked loan framework encourages registration, documentation, and structured financial records. This process integrates informal enterprises into the formal banking system, enabling them to build credit profiles and long-term financial credibility.

3. Expansion Support

The initiative provides capital for working capital needs, equipment acquisition, inventory expansion, and operational upgrades. By improving access to funds, businesses can increase production capacity, hire additional staff, expand into new markets, and improve service delivery.

4. Non-Interest Option

For entrepreneurs seeking ethical or Sharia-compliant financing, the partnership with Jaiz Bank offers a non-interest alternative. This structure allows business owners to access funding through profit-sharing or asset-backed models rather than conventional interest-based lending.

5. National Economic Impact

Beyond individual businesses, the initiative contributes to broader economic growth. Increased MSME financing supports job creation, enhances productivity, stimulates local manufacturing and trade, and strengthens Nigeria’s overall economic resilience.

Together, these advantages make the SMEDAN Sterling Loan Initiative a strategic tool for empowering small businesses while advancing national development objectives.

Safety Tips When Applying

Because of the strong demand for MSME financing in Nigeria, fraudulent actors sometimes exploit entrepreneurs by creating fake portals, impersonating officials, or promising guaranteed approvals. When applying for a SMEDAN loan, whether through Small and Medium Enterprises Development Agency of Nigeria partnerships with Sterling Bank or Jaiz Bank, it is important to take deliberate precautions to protect your business and personal information.

Below are essential safety guidelines every applicant should follow:

Use Official Bank Websites Only

Always access the loan application through verified official websites of the partner bank or SMEDAN. Avoid clicking on random social media links, WhatsApp broadcasts, or unofficial emails claiming to offer the SMEDAN Sterling loan application. Fraudulent websites often imitate official branding but may have slightly altered web addresses. Before entering sensitive information such as BVN or bank details, confirm that the website URL is legitimate and secure (look for “https” and proper domain spelling).

Avoid “Guaranteed Approval” Agents

No legitimate SMEDAN-linked loan guarantees automatic approval. Loan approval depends on credit assessment, documentation review, and financial evaluation by the partner bank. Be cautious of individuals who claim they can “fast-track” or “guarantee” approval for a fee. Such promises are strong warning signs of fraud. Official programs follow structured assessment procedures and do not rely on middlemen.

Do Not Pay Unofficial Processing Fees

Reputable loan programs clearly state their official charges (if any). You should never be asked to transfer money into a personal account to “secure” your loan. Scammers often demand advance payments disguised as processing fees, insurance charges, or approval tokens. Always confirm payment instructions directly from the official bank platform before making any transaction.

Verify the SMEDAN/Sterling Bank Loan Registration Portal

Before completing your SMEDAN loan login or uploading documents, confirm that you are using the correct SMEDAN/Sterling Bank loan registration portal. Cross-check the link through the official website or contact the bank’s customer service line if unsure. Never share sensitive information such as your BVN, OTP codes, or login credentials with third parties.

Frequently Asked Questions (FAQ)

Here are some frequently asked questions about SMEDAN loans.

Is SMEDAN loan a grant?

No. It must be repaid according to agreed terms.

Do I need SMEDAN registration loan status before applying?

Yes. SMEDAN registration strengthens eligibility.

Is there a SMEDAN CBN loan application form?

Some funding aligns with CBN-backed frameworks, but applications are processed through partner banks.

Can I apply without CAC registration?

No. Legal business registration is required.

What is the SMEDAN Sterling Bank loan interest rate?

Rates vary and should be confirmed via official channels.

How long does approval take?

Processing time depends on documentation and verification.

Can startups apply?

Yes, but financial viability must be demonstrated.

Final Thoughts

The SMEDAN Sterling loan application initiative represents a strategic effort to bridge Nigeria’s MSME financing gap. Through partnerships with Sterling Bank and Jaiz Bank, structured credit becomes more accessible to legitimate businesses.

However, success depends on proper CAC registration, active SMEDAN registration, accurate documentation, responsible borrowing, and realistic financial planning

For Nigerian entrepreneurs asking “How do I apply for SMEDAN loan?” or “How can I access my SMEDAN loan?”, the key lies in preparation, compliance, and using only official portals.

When used responsibly, SMEDAN-linked financing can support sustainable business growth, expansion, and long-term economic contribution.